People often ask, “What is the best way to pass oil and gas mineral interests to a son, daughter, spouse, or grandchild?” The answer depends on your family’s unique circumstances. Options include using a Last Will, Trust, or Transfer on Death Deed. Others may consider granting a deed or creating a life estate. However, there is no one-size-fits-all solution.

The best approach is to carefully review these options with an experienced estate planning attorney, who can help tailor a plan to meet your goals and avoid unnecessary legal hurdles like probate.

Mineral Inheritance and Family Legacy

Mineral ownership is distinct because it often passes through generations, preserving a family legacy. In Oklahoma, it’s common for mineral rights to trace back to a land run or homestead deed. Sometimes, surface rights were sold, but families retained the mineral rights as a connection to their land.

During the Dust Bowl, many Oklahomans who moved away kept their mineral interests with the hope that homesteading dreams will pay off. Many descendants are now benefiting from their ancestors’ forethought. As a current mineral owner, you can honor this tradition by thoughtfully planning how to pass these rights to the next generation.

This article explores common methods for transferring mineral interests, including strategies to avoid probate. While the examples primarily focus on passing rights to children, these methods also apply when leaving mineral rights to a spouse or another beneficiary.

Probate Process and Minerals

In Oklahoma, probate is a judicial process used to settle the estate of a deceased individual (decedent). This legal procedure is necessary if the decedent had a Last Will and Testament or died without a will (intestate) and the property does not pass through a non-probate transfer, such as a Trust or Transfer on Death Deed.

The probate process involves several steps:

- Notification: Notice is provided to heirs (those entitled to inherit) and creditors.

- Appointment: A personal representative (executor) is appointed by the court to manage the estate.

- Notices and Publications: Required notices must be mailed and published to inform interested parties.

- Debt and Taxes: The personal representative pays creditors and any applicable taxes.

- Distribution: Remaining property is distributed according to the decedent’s Will or, if there is no Will, according to Oklahoma intestacy laws.

While probate will eventually ensure that titles are cleared and royalties are placed into pay status, it is often considered a costly and time-consuming process. For this reason, many individuals prefer to use non-probate planning tools to simplify the transfer of assets and avoid unnecessary legal headaches.

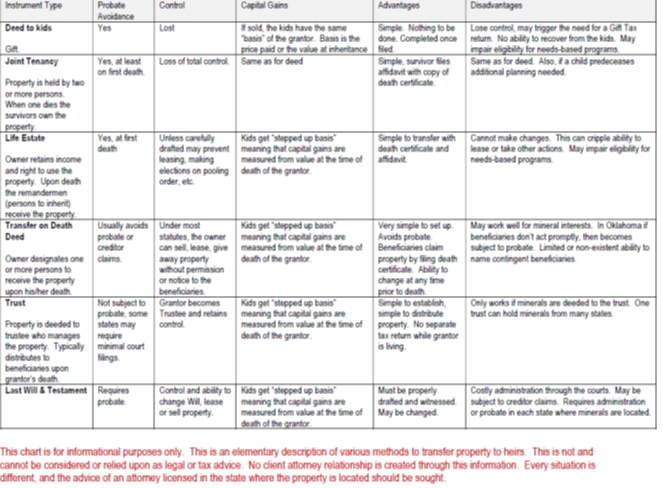

Deeds for Mineral Interests

Another way to pass property is through a deed. These can be one of many forms.

1. Outright Mineral Deed

A parent can transfer mineral rights directly to a child using a quit claim mineral deed. Once executed, the child owns the property outright and is entitled to all associated income.

Potential Drawbacks:

Creditor Risks: The mineral rights may become vulnerable to the child’s creditors, bankruptcy, or claims from a divorcing spouse.

Loss of Control: The parent relinquishes all rights and decision-making power over the property.

Impact on Assistance: Transferring assets may disqualify the parent from nursing home assistance or veteran’s benefits.

Tax Implications: If the child sells the property, they may face capital gains taxes that could have been avoided. A transfer may also trigger gift tax considerations.

Joint Tenancy Mineral Deed:

A joint tenancy deed places mineral ownership into the names of two or more individuals, using language like:

“To A & B as joint tenants with rights of survivorship and not tenancy in common.”

This is common for married couples. When one owner dies, their interest automatically transfers to the surviving owner(s) by filing an affidavit.

Potential Drawbacks:

- Similar risks as an outright deed, including creditor claims, bankruptcy, or divorce complications for the child.

- Loss of control by the parent once the property is jointly owned.

. More about Joint Tenant Deed Here.

Mineral Life Estate:

A life estate deed allows a parent (the life tenant) to retain royalties and control during their lifetime. The property is deeded to children (the remaindermen), who take ownership after the parent’s death by filing an affidavit.

Potential Challenges:

- Waste Prohibition: The life tenant cannot take actions that impair the property’s value for the remaindermen.

- Leasing Issues: Life tenants may need consent from remaindermen to sign leases or make elections under a pooling order.

- Drafting Complexities: While careful drafting can mitigate some issues, the cost of creating a life estate often outweighs the benefits compared to a trust.

Transfer on Death Mineral Deed

A Transfer on Death (TOD) Mineral Deed is a simple and flexible way to designate beneficiaries to inherit mineral rights. The process involves signing the deed, having it witnessed, and filing it with the county land records where the minerals are located.

Key Features of a TOD Mineral Deed:

- Owner Retains Control: The owner can lease, sell, rent, gift, or even revoke the TOD deed without notifying the beneficiaries.

- Beneficiary Designation: Beneficiaries inherit the property only after the owner’s death.

How It Works:

- Upon the owner’s death, the beneficiary becomes the owner by filing an affidavit along with a death certificate.

Potential Drawbacks of TOD Mineral Deeds

- Deadline to Claim Ownership:

- The beneficiary must file an affidavit within 9 months of the owner’s death to claim the property.

- Missing this deadline means the property becomes part of the owner’s probate estate.

- No Contingent Beneficiaries:

- Oklahoma law does not allow for contingent beneficiary designations.

- If a named beneficiary predeceases the owner, their inheritance lapses. For example, a provision like “to my son, but if my son does not survive me, then to his children” will not work under current law.

Conclusion

While a Transfer on Death Mineral Deed offers flexibility and simplicity, it has limitations that may not suit every situation. For those needing contingency planning or wanting to avoid probate complications, a trust might be a better option. Consulting an experienced estate planning attorney ensures the best approach for your family’s needs and goals.

More about Transfer on Death Deeds Here.

Trusts for Oil and Gas Interests

A trust is an effective way to hold and manage oil and gas interests, providing multiple benefits, including avoiding probate and offering protection for beneficiaries. Here’s a detailed look at how trusts work for mineral rights and oil and gas assets.

What Is a Trust?

A trust is a legal arrangement where a trustee holds title to property for the benefit of designated beneficiaries. Key components include:

- Trust Document: Establishes the trust’s rules, names the trustee(s), successor trustee(s), and beneficiaries.

- Trustee Control: The initial trustee (often the property owner) retains full control during their lifetime, including leasing, selling, or making pooling order elections.

- Successor Trustees: Take over management upon the death or incapacity of the original trustee.

- Beneficiary Designations: Specify who will inherit or benefit from the property, including contingency plans if a beneficiary predeceases the owner.

Key Benefits of a Trust for Oil and Gas Interests

- Avoiding Probate:

- A properly funded trust bypasses the time-consuming and costly probate process.

- This ensures a smooth transfer of ownership to beneficiaries.

- Flexibility and Control:

- The owner maintains control of the assets during their lifetime.

- Provisions can be included to handle contingencies, such as passing assets to grandchildren if a beneficiary predeceases the owner.

- Protection from Creditors:

- Trusts can shield assets from beneficiaries’ creditors, bankruptcy, or divorcing spouses.

- Exceptions: Claims for child support or taxes are not protected.

- Special Needs Trusts:

- For family members with disabilities or those on needs-based programs like SSI or Medicaid, a Special Needs Trust can safeguard the inheritance without jeopardizing their eligibility for benefits.

Tax Implications and Management

- During the Owner’s Lifetime: There is no need for a separate tax return; the trust income is typically reported under the owner’s social security number.

- After Death: The trust may require its own tax identification number, depending on its structure and provisions.

Customizing the Trust for Minerals

- Simple Trusts: The trustee may be required to transfer mineral deeds directly to beneficiaries upon the owner’s death.

- Management Trusts: Designed to continue managing oil and gas assets for the benefit of beneficiaries, providing long-term oversight.

Important Considerations

- Rule Against Perpetuities: Trusts for minerals must comply with rules requiring assets to vest outside the trust within a specific timeframe. This ensures that the trust does not last indefinitely.

Special Needs Trusts for Vulnerable Beneficiaries

For individuals receiving SSI or Medicaid, a Special Needs Trust can:

- Protect inherited assets from being counted as resources that could disqualify them from benefits.

- Ensure access to essential programs such as housing and medical care.

Why Use a Trust for Oil and Gas Interests?

A trust is a powerful estate planning tool that provides flexibility, protection, and efficiency. It’s particularly valuable for families with complex inheritance goals or vulnerable beneficiaries. A simple trust is often less expensive than the cost of probate and provides greater control over how assets are distributed.

Consulting with an experienced estate planning attorney ensures the trust is properly structured and funded to meet your family’s needs.

Limited Liability Company (LLC) for Mineral Interests

An LLC can be a practical tool for managing and passing down mineral interests, especially for individuals with high-net-worth or for families owning mineral rights in multiple states. Here’s a detailed look at using an LLC for mineral ownership.

What Is an LLC?

A Limited Liability Company (LLC) is a legal entity that allows individuals to hold and manage assets like mineral rights. It combines the liability protection of a corporation with the operational flexibility of a partnership.

Key Features of an LLC for Mineral Rights

- Ownership Across States:

- An LLC can own mineral rights in multiple states but must register in each state where the minerals are located.

- Registration includes filing with the Secretary of State and paying annual fees.

- Reporting Requirements:

- Annual reports and fees are required to maintain good standing in each state.

- A registered office with a physical street address (no P.O. Boxes) must be maintained in every state of registration.

- Ownership Structure:

- Units, similar to stock, represent ownership in the LLC.

- Different classes of membership (e.g., voting and non-voting) allow flexibility in control and decision-making.

- Management:

- A designated manager operates the LLC, handling leases, royalties, and other transactions.

Advantages of an LLC for Mineral Interests

- Liability Protection:

- Owners (members) are shielded from personal liability for debts or obligations of the LLC.

- Tax Benefits for High-Net-Worth Individuals:

- Annual gifting of units can be used to transfer ownership incrementally to the next generation, potentially reducing estate tax exposure.

- Centralized Management:

- An LLC provides a streamlined way to manage mineral assets, particularly when ownership is fragmented among family members or generations.

- Flexibility in Ownership:

- Voting and non-voting membership options allow for tailored control, such as parents retaining operational authority while transferring financial benefits to children.

Limitations of Using an LLC

- Complexity:

- Setting up and maintaining an LLC requires ongoing administrative work, including filings, fees, and compliance with state regulations. The Corporate Transparency Act also requires reporting and keeping records up to date.

- Tax and Reporting Requirements:

- Unlike a trust, an LLC may require additional tax filings, depending on its structure and income.

- Mechanism for Passing Ownership:

- An LLC does not inherently transfer ownership upon death. A companion tool, like a trust, is often necessary to ensure a smooth transition to heirs without probate.

- Not Ideal for Small Estates:

- For individuals with modest holdings or those unfamiliar with managing a formal organization, a trust may be a simpler and more cost-effective option.

When to Consider an LLC

- High-Net-Worth Individuals:

- For those with significant mineral holdings, an LLC offers robust options for managing ownership and tax advantages.

- Multiple Heirs or Generational Planning:

- An LLC can help avoid disputes among family members by centralizing management and clearly defining ownership roles.

- Multi-State Ownership:

- If mineral rights span multiple states, an LLC can consolidate management and simplify the administrative burden.

LLCs and Trusts Together

- Why Combine?:

- A trust can hold LLC units, enabling the avoidance of probate and ensuring a seamless transfer of assets upon the owner’s death.

- This combination leverages the flexibility and control of an LLC with the estate planning benefits of a trust.

Conclusion

While an LLC offers liability protection, centralized management, and tax planning benefits, it is best suited for high-net-worth individuals or families with complex holdings. For most individuals, a trust is a simpler and more effective solution.

Consulting an estate planning attorney familiar with mineral rights can help determine if an LLC, a trust, or a combination of both is the right fit for your situation.

Last Will and Testament and Oil and Gas

A Last Will and Testament is a legal document that allows a person (the testator) to designate how their property, including oil and gas interests, will be distributed after their death. While it offers flexibility, there are critical considerations to keep in mind when dealing with mineral rights.

Key Features of a Last Will and Testament for Mineral Rights

- Disinheritance:

- Except for a spouse, the testator can legally disinherit any family member.

- Specific Gifts:

- A Will can specify that particular mineral interests go to designated individuals, such as a child or grandchild.

- Alternatively, it can distribute the remainder of the estate (including minerals) using a formula, such as dividing the property equally among beneficiaries.

- Statutory Compliance:

- To be valid, a Will must meet all legal requirements, including proper witnessing and signing.

- Oral Wills or informal written documents, even if they clearly express the testator’s intentions, are not valid.

- Probate Required:

- A Will does not avoid probate.

- The probate process is necessary to prove the Will’s validity and transfer title to heirs or beneficiaries.

Why a Will May Not Be Ideal for Mineral Rights

- Probate Challenges:

- The probate process can be costly and time-consuming, particularly for mineral interests located in multiple counties or states.

- During probate, royalties may be placed in suspense, delaying payments to heirs.

- Lack of Flexibility:

- A Will does not provide mechanisms to manage the property after the testator’s death.

- For example, it cannot protect the inheritance from creditors or provide for contingencies like a beneficiary predeceasing the testator.

Considerations for Mineral Rights in a Will

Decide if the minerals should be divided equally among beneficiaries or gifted to a specific person.

More about Last Will and Testament Here.

If you choose to include mineral rights in your Will, ensure it is clear and detailed:

Specify the exact legal description of the mineral interests to avoid ambiguity.

Power of Attorney and Mineral Interests

A Power of Attorney (POA) is a vital document in managing mineral rights, particularly when the owner may face incapacity. It grants a trusted individual (the agent) the authority to act on behalf of the principal (the person creating the POA).

Key Features of a Power of Attorney for Mineral Interests

In such cases, the court may appoint a guardian or conservator, which is a time-consuming and costly process.

Purpose and Limitations:

A POA is only effective while the principal is alive.

It cannot be used to distribute property or handle estate matters after death.

Use in Incapacity:

If the principal becomes mentally or physically incapacitated, the agent can act on their behalf.

This authority includes signing oil and gas leases, making elections under pooling orders, or managing royalty payments.

Avoiding Guardianship:

Without a valid POA, no one would have the legal authority to manage the principal’s mineral interests during incapacity.

Beware of Online Forms

In today’s digital age, many legal forms, including estate planning documents, can be easily found online for free or for a nominal fee. While this may seem convenient and cost-effective, relying on these forms can lead to serious problems that may not surface until it’s too late to correct them.

Common Problems with Online Legal Forms

- Choosing the Wrong Form:

- Legal documents vary by jurisdiction, and a form that works in one state may not be valid in another.

- Online forms often fail to account for state-specific requirements, especially for complex matters like mineral interests or trust creation.

- Improper Completion:

- Legal terminology and processes can be confusing.

- Errors in completing the form—such as omitting key details or misunderstanding legal terms—can render it ineffective or invalid.

- Improper Witnessing:

- Many legal documents, such as wills or powers of attorney, require witnesses and/or notarization.

- Failing to follow these requirements exactly as specified by state law can invalidate the document.

- Failure to File or Record:

- Certain documents, such as deeds or mineral transfers, must be properly filed with the appropriate government office.

- Neglecting this step can leave the intended actions incomplete, requiring additional legal proceedings to resolve.

The Consequences of Mistakes

- Incapacity Issues:

- If a power of attorney or healthcare directive is invalid, no one may have the legal authority to act on behalf of the individual during incapacity.

- This could lead to costly and time-consuming court proceedings for guardianship or conservatorship.

- Probate Challenges:

- Errors in wills or trust documents may lead to probate disputes, delays, and unintended distributions.

- Irrevocable Loss:

- Once an individual becomes incapacitated or passes away, it’s often impossible to correct mistakes or omissions in their documents.

Why Work with an Experienced Attorney?

With professionally prepared documents, you can rest assured that your estate plan is valid and enforceable, reducing the risk of disputes or complications.

Tailored Advice:

An attorney can provide personalized guidance based on your unique circumstances, ensuring that the documents align with your goals and comply with state laws.

Preventative Measures:

Attorneys can anticipate and address potential issues, such as contingencies for predeceased beneficiaries or tax implications.

Proper Execution:

Legal professionals ensure documents are properly executed, witnessed, notarized, and, if necessary, filed or recorded with the appropriate entities.

Peace of Mind:

Conclusion:

There is no universal “best” way to transfer mineral interests or other property to beneficiaries. Each situation requires careful consideration of the owner’s goals, the beneficiaries’ needs and capabilities, and the available budget. Estate planning solutions must be tailored to ensure they meet these unique requirements while avoiding unnecessary complications or costs.

This article serves as an overview of the topic, offering insight into some of the methods and considerations involved in estate planning. However, it is not intended to be used as legal or tax advice. Before making any decisions or executing estate planning documents, consult with a qualified attorney who specializes in estate planning and probate. Professional guidance ensures that your plan aligns with your objectives, complies with the law, and protects your legacy.