A financial power of attorney (POA) is a legal document that grants a person you trust the authority to manage your financial affairs if you become unable to do so yourself. This can include anything from paying monthly bills and managing investment accounts to selling real estate or filing taxes. Because it is a “durable” power of attorney, the authority remains in effect even if you become mentally or physically incapacitated.

Why is a Financial Power of Attorney Important?

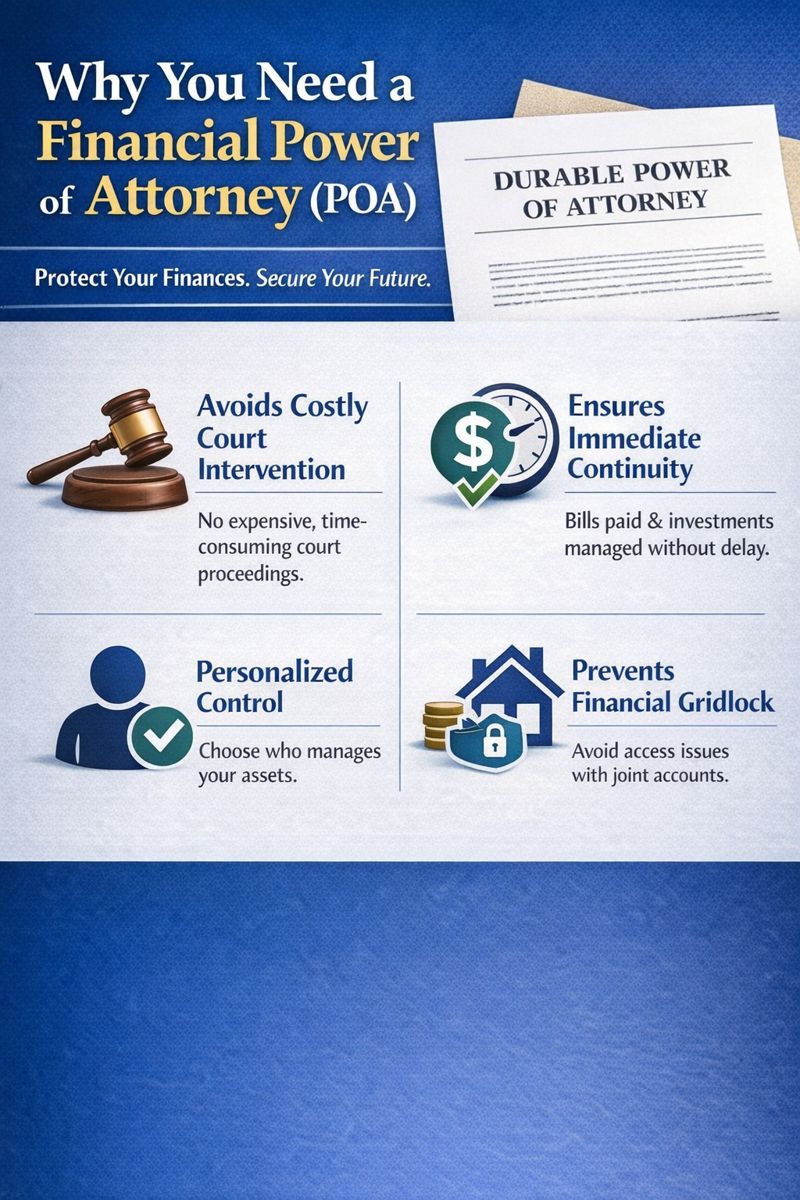

The primary reason to have a POA is to maintain control over your future. Without this document, your family is often left in a legal “limbo.” If you cannot sign your name or make decisions, your bank accounts and assets may be effectively frozen. A POA provides the legal key for a loved one to step in and keep your financial life moving without interruption.

Preventing Family Conflict: Who is in Charge?

One of the most common issues we see in our concentrated practice is family infighting when a plan isn’t in place. Without a POA, siblings or relatives may disagree on who should handle your money or how it should be spent. This “power vacuum” often leads to:

- Costly Litigation: Family members may sue for guardianship or conservatorship.

- Irreparable Relationships: Disputes during a crisis often leave lasting scars on family dynamics.

By clearly designating who is in charge, you eliminate any ambiguity and ensure that your hand-picked agent has the sole authority to act on your behalf.

How a Financial POA Protects Your Assets

A properly drafted POA ensures that your mortgage, insurance, retirement and taxes are paid on time, protecting your credit and preventing foreclosure or a lapse in coverage. Our firm offers focused experience in drafting these essential documents to ensure they are legally sound and tailored to your specific goals.

What Powers Can a Financial POA Grant?

A financial power of attorney is not a “one-size-fits-all” document. Through our focused experience in estate planning, we help clients tailor these powers to their specific needs. Depending on how the document is drafted, an agent can be granted the authority to:

- Manage Real Estate: Buy, sell, lease, or mortgage property on your behalf.

- Handle Banking Transactions: Deposit checks, withdraw funds, and open or close accounts.

- File Tax Returns: Sign and file federal and state taxes and represent you before the IRS.

- Manage Retirement Benefits: Handle distributions or elections for Social Security, Medicare, or military benefits.

- Oversee Investments: Trade stocks, bonds, and manage mutual fund accounts.

- Operate a Business: Continue the day-to-day operations of a family-owned business or professional practice.

Can’t My Spouse Just Handle Things?

This is one of the most common questions we hear in our concentrated practice. Many people assume that a marriage license automatically grants full financial authority, but that is a dangerous misconception. Here is why a spouse often lacks the legal standing to act alone:

- Separate Bank Accounts: If you have an account in your name only, your spouse cannot access those funds to pay bills or mortgage payments without a POA or a court order.

- Retirement Accounts (IRA/401k): By law, retirement accounts are individual. Your spouse cannot change your contribution amounts, manage your investments, or make required minimum distribution (RMD) elections for you unless they are your designated agent.

- Real Estate Transactions: Even if you own a home together, you generally cannot sell or refinance a property if one owner is incapacitated. Both signatures are typically required for a deed or mortgage; without a POA, the healthy spouse is often stuck in legal gridlock.

- Insurance and Contracts: Your spouse may be unable to cancel or modify insurance policies, cell phone plans, or other contracts that are in your name only.

Can You Get a POA for Someone with Declining Capacity, Dementia, Alzheimers?

The short answer is yes, but only if the person still has “testamentary capacity.” In Oklahoma, the legal standard for signing a contract (which applies to a POA) is actually stricter than the standard for signing a will.

The individual must be able to understand:

- The nature and effect of the document they are signing.

- The extent of the property and assets they own.

- The specific powers they are granting to their chosen agent.

If a person has advanced dementia or is no longer “of sound mind,” they can no longer legally sign a POA. At that point, the family’s only option is often to petition the court for Guardianship, which is more expensive, time-consuming, and takes the decision-making power out of your hands and puts it into the hands of a judge.

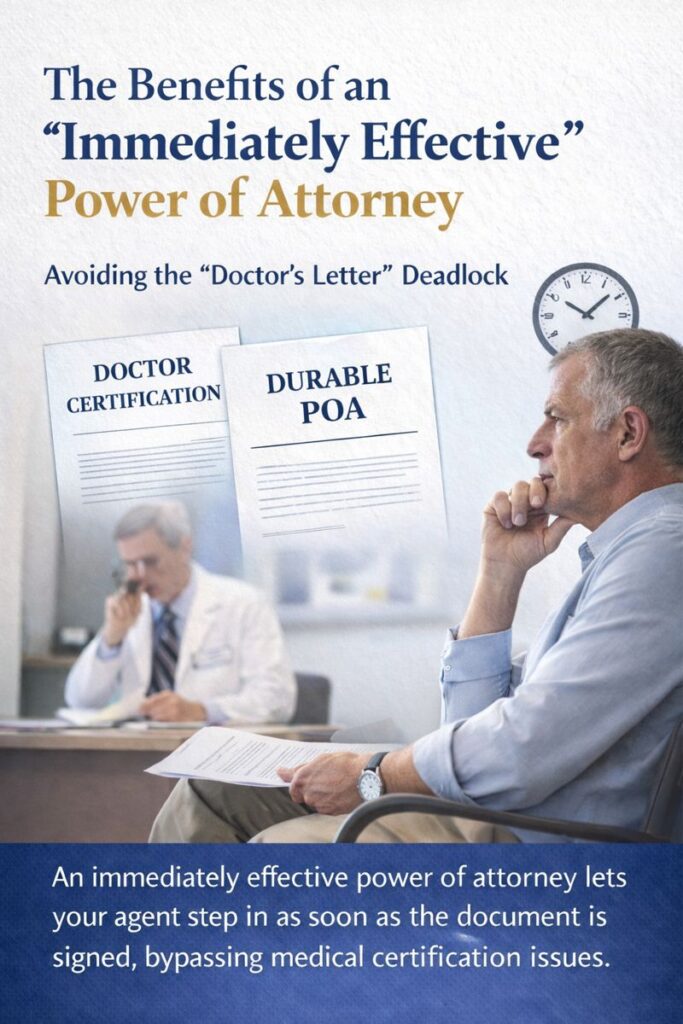

The Benefits of an “Immediately Effective” Power of Attorney

When creating a financial power of attorney, you must decide when the document becomes active. You can choose a “Springing” POA, which only takes effect upon a certified medical crisis, or a “Durable” POA that is effective immediately upon signing. While many people like the idea of their agent only having power once they are incapacitated, the practical hurdles of a springing document can cause significant delays.

Avoiding the “Doctor’s Letter” Deadlock

A springing POA requires a “triggering event”—usually a written certification of your incapacity by one or more physicians. In a crisis, this can lead to several problems:

- Physician Reluctance: Doctors are often hesitant to sign formal letters of incapacity. They are keenly aware of the legal weight such a letter carries regarding your autonomy and may be reluctant to sign a document that could potentially be used in family litigation.

- The Search for a Second Opinion: Many springing documents require two doctors to sign off. If you are in a care facility or hospital, finding a second doctor willing to perform a capacity assessment on short notice can be difficult, expensive, and time-consuming.

- Timing and Delays: It can take days or weeks to coordinate medical assessments and obtain written letters. During that time, your mortgage, insurance, and medical bills may go unpaid because your agent technically has no power to act until the paperwork is finalized.

An immediately effective power of attorney helps avoid delays caused by required medical certifications during a crisis.

Overcoming Third-Party Hurdles

One of the most persistent issues with a springing POA is the “Proof of Incapacity” requirement from banks and financial institutions. Even if you have a valid document, third parties often create obstacles that an immediately effective document avoids.

- The Requirement for “Fresh” Evidence: Even if you have a doctor’s letter, a bank may refuse to honor it if the finding of incapacity is not recent enough. If your condition is degenerative, a bank may demand updated medical findings every few months or years to prove the “springing” power is still active. This creates a recurring administrative burden for your family during an already stressful time.

- Immediate Verification: With an immediately effective document, the agent’s authority is not tied to your health status. This allows your agent to visit your bank before a crisis occurs, present the document, and ensure the bank’s legal department has approved it. When the time comes that you actually need help, the “red tape” has already been cleared.

The “Safety Net” Approach

Choosing an immediately effective POA does not mean you lose your right to handle your own affairs. It simply means the “safety net” is already deployed. You can keep the original document in a safe place, only giving it to your agent when you feel the time is right. This provides the protection of immediate action without the administrative nightmare of proving a medical crisis to a skeptical third party.

The Mistake of “Equal” Treatment: Why Naming Multiple Co-Agents Can Fail

When parents create a financial power of attorney, they often feel a strong desire to treat all their children “equally.” This frequently leads to naming two or more children as co-agents, expecting them to work together. While well-intentioned, this decision can inadvertently create the very conflict and “power vacuum” the document was designed to avoid.

The Risk of Decision Deadlock

When you name co-agents, you typically must decide whether they must act jointly (meaning they must both agree and sign every document) or independently (meaning either can act alone). Both setups have significant drawbacks:

- Joint Authority Hurdles: Requiring two or more people to agree on every single financial decision—from paying a utility bill to selling a home—is a recipe for paralysis. If your children disagree on a course of action, the result is a deadlock. In many cases, the only way to break a deadlock between co-agents is to go to court, which is expensive, public, and often permanently damages family relationships. Naming an odd number thinking it will resolve deadlocks. For example, if there are three agents and 3 choices then there can still be deadlock.

- Independent Authority Chaos: If you allow co-agents to act independently, you risk a “decision loop.” One child might pay a bill or sell a stock while the other, unaware of the first child’s actions, attempts to do the same or undo it. This lack of coordination can lead to accounting nightmares and confusion for your banks and creditors.

Third-Party Confusion and Refusal

Banks and financial institutions are highly sensitive to fraud and internal disputes. When multiple agents are involved, third parties often become hesitant to cooperate.

- “Too Many Cooks”: If two different people show up at a bank with the same power of attorney but give conflicting instructions, the bank’s typical response is to freeze the account until a court order tells them who to listen to.

- Verification Burdens: Every time a transaction is made, the bank may require proof that all agents are still serving or that they have consulted one another. This “red tape” defeats the purpose of having a POA to make life easier during a crisis.

Successor Agents: A Better Way to Show Trust

Treating children “fairly” does not have to mean giving them “equal” authority at the same time. A more effective approach is naming a primary agent followed by successor agents in a specific order.

- Clear Chain of Command: By naming a primary agent (perhaps the child with the most financial experience or the one who lives closest), you ensure there is one clear voice in charge. This eliminates the risk of a power vacuum or sibling stalemate.

- The Backup System: Naming the other children as successors shows that you trust them and have a plan in place if the primary agent is unavailable or unable to serve.

Choosing a single person to be “the lead” isn’t an act of favoritism; it is a practical step to ensure your finances stay protected and your family stays out of court.

The Oklahoma Guide to Financial Power of Attorney: Protecting Your Assets and Family

A financial power of attorney (POA) is one of the most critical documents in a comprehensive estate plan. While many people focus on what happens after they pass away, a POA is a “living” document designed to protect you, your assets, and your family’s harmony while you are still here.

What is the Oklahoma Uniform Power of Attorney Act?

In Oklahoma, financial powers of attorney are governed by the Oklahoma Uniform Power of Attorney Act (UPOAA). This law provides a clear framework for how these documents must be created and how agents must behave. Under this Act, a power of attorney is presumed to be “durable,” meaning it remains valid even if you become mentally or physically incapacitated, unless the document specifically states otherwise.

The Power of Portability: The Oklahoma Uniform Power of Attorney Act

One of the most important aspects of estate planning in the modern age is “portability.” In 2021, Oklahoma modernized its laws by adopting the Oklahoma Uniform Power of Attorney Act (UPOAA). Oklahoma is part of a growing majority, as over 30 states (including neighboring Texas, Arkansas, and New Mexico) have now adopted this uniform legislation.

Why Uniformity Matters for You

Before the UPOAA, power of attorney laws varied wildly from state to state. A document drafted in Oklahoma might have been rejected by a bank in Florida or a title company in Arizona because the wording didn’t match their local statutes.

By using a document based on the UPOAA, you gain several advantages:

- Ease of Acceptance Across State Lines: Because so many states now use the same legal “language” and standards, your Oklahoma POA is much more likely to be recognized and accepted immediately by out-of-state institutions. This is vital if you own a vacation home, hold out-of-state investments, or if you relocate for retirement.

- Mandatory Acceptance by Third Parties: One of the strongest features of the Act is that it encourages third parties (like banks and insurance companies) to accept the document. Under Oklahoma’s version of the Act, a third party that refuses an acknowledged (notarized) POA without a valid legal reason can actually be held liable for attorney’s fees and costs incurred in a court action to confirm the document’s validity.

About Richard Winblad

In the complex world of Oklahoma estate law, technical details are the difference between a secure legacy and a family legal battle. Richard Winblad brings a concentrated practice in estate planning, probate, and trust law to every client he serves, ensuring that their intentions are translated into legally sound documents.

As an active member of the Oklahoma Bar Association’s Estate Planning, Probate, and Trust Section, Richard stays at the forefront of the statutes that govern the transition of assets between generations. His commitment to legal excellence earned him the “Award of Excellence” for his contributions to the professional handbook for Medicaid and Long-Term Care Planning—a vital resource used by attorneys throughout the state.

Richard is also a dedicated educator within the legal profession. He has authored and taught Continuing Legal Education (CLE) classes for fellow Oklahoma Bar members, sharing his insights on navigating the intricacies of probate and trust management. Beyond his work with other attorneys, he frequently presents to non-profit organizations, professional groups, and the public to help Oklahomans understand that a verbal promise cannot substitute for a properly executed plan.

Peer Recognized for Professional Excellence

Our commitment to providing clear, honest guidance—treating every client with the same integrity I would show a member of my own family—is reflected in my AV Preeminent® peer review rating from Martindale-Hubbell.

This rating is the highest distinction a lawyer can achieve and is a testament to the fact that my fellow attorneys and members of the judiciary rank my work at the highest level of professional excellence.*

Mandatory Disclaimer

Note on Ratings: AV®, AV Preeminent®, Martindale-Hubbell Distinguished and Martindale-Hubbell Notable are certification marks used under license in accordance with the Martindale-Hubbell certification procedures, standards and policies. Martindale-Hubbell® is the facilitator of a peer review rating process. Ratings reflect the anonymous opinions of members of the bar and the judiciary. Martindale-Hubbell® Peer Review Ratings™ fall into two categories – legal ability and general ethical standards. This is not a certification of any specialty.