Protecting your family’s future and ensuring your legacy is handled with dignity requires more than just a simple document; it requires a comprehensive strategy. At Winblad Law, we bring focused experience to the creation of custom-tailored plans that provide clarity and security for Oklahoma families. Whether your goal is to avoid the public probate process, manage complex mineral interests, or ensure your healthcare wishes are honored, a well-crafted plan is the greatest gift you can leave your loved ones. Below are the essential components of a proactive estate plan designed to protect your assets and provide you with lasting peace of mind.

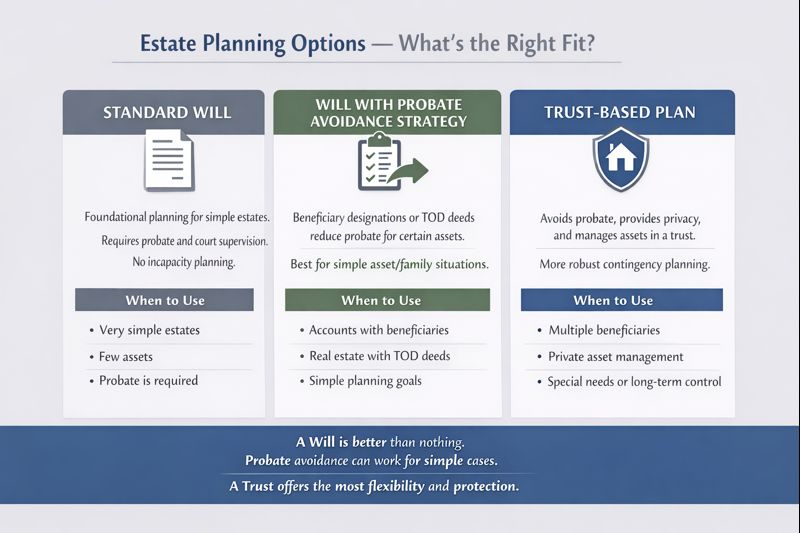

Most people believe estate planning is only for the wealthy, but in Oklahoma, having the right plan can save your family from a public and costly court process. While both Wills and Trusts allow you to decide who receives your assets, they function very differently under Oklahoma law.

In Oklahoma, this is usually the deciding factor for most families:

| Feature | Last Will & Testament | Revocable Living Trust |

| Effective Date | Upon death | Immediately |

| Probate Required? | Yes | No (if properly funded) |

| Privacy | Public Record | Private |

| Incapacity Planning | None (requires Guardianship) | Built-in (Successor Trustee) |

| Setup Cost | Generally lower upfront | Generally, slightly higher upfront |

| Administration Cost | Higher (Attorney & Court fees) | Lower (Private administration) |

If your primary goal is to keep your home, car, and bank accounts out of the Oklahoma probate courts, you can use “non-testamentary” transfers. These tools move assets directly to your heirs the moment you pass away.

While these options are low-cost and simple to set up, they should be used with extreme caution. Unlike a trust, these designations are “rigid” and cannot account for life’s “what-ifs.”

Relying solely on these “automatic” transfers is often a gamble. At Winblad Law, we have seen these shortcuts fail for several reasons:

While TODs and PODs are useful tools, they are components of a plan, not a replacement for a comprehensive strategy. If you have minor children, blended family concerns, or want to protect your heirs from creditors and divorce, a trust is almost always the more secure route.

Asset Type | The Tool | How it Works in Oklahoma |

| Real Estate | TOD Deed | You record a deed now; it transfers only at death. The beneficiary must file an acceptance affidavit within 9 months. |

| Retirement (IRA/401k) | Beneficiary Designation | Managed directly through your plan administrator. These funds bypass your Will and are paid directly to the named person. |

| Life Insurance | Beneficiary Designation | The death benefit is paid contractually to your heirs. It is generally not subject to the debts of your probate estate. |

| Bank Accounts | POD Designation | A simple contract with your bank. You retain 100% control while alive; heirs claim funds with a death certificate. |

| Vehicles | Service Oklahoma TOD | You file a notice with Service Oklahoma. The title remains in your name but transfers automatically upon death. |

https://calendly.com/winbladlaw/estate-planning-meeting

When someone passes away without a Will in Oklahoma, they are said to have died “intestate.” This means that instead of you deciding who receives your property, the State of Oklahoma decides for you based on a rigid legal formula.

At Winblad Law, we see many families surprised to learn that “everything going to the spouse” is a common misconception in Oklahoma law. In many cases, the state actually divides your assets between your spouse and other relatives.

The distribution of your estate depends entirely on which family members survive you at the time of your death.

Dying without a plan doesn’t just change who gets your assets; it changes how they get them, often leading to unnecessary stress for your loved ones.

Read about the cautionary tale of the failed estate plan.

To understand the risk of dying without a plan, we can look at one of the most famous examples in American history: Hollywood icon James Dean.

James Dean’s life was marked by a complex family structure. After his mother passed away when he was only nine years old, Dean became estranged from his father. He was sent to live with an aunt and uncle on a farm in Indiana, and they were the ones who truly raised him and supported his early career.

When Dean died tragically at age 24 in a car accident, he had no Will. Because he died “intestate,” the law (similar to Oklahoma’s current statutes) ignored his close relationship with his aunt and uncle and looked strictly at his legal bloodline.

Despite their years of estrangement, James Dean’s entire estate—and the ongoing rights to his lucrative likeness—passed directly to his father. While we cannot know for certain what Dean would have wanted, it is highly likely he would have preferred to provide for the relatives who raised him rather than the father he barely knew. Without a legal document to state those wishes, the court had no choice but to follow the rigid rules of succession.

The James Dean story isn’t just for celebrities; it happens to Oklahoma families every year. Intestacy laws cannot account for:

Oklahoma’s intestacy laws are a “one-size-fits-all” safety net, but they rarely match a family’s true wishes or unique dynamics. Whether you have a complex estate or a simple family structure, having a plan ensures that you remain in control of your legacy.

Read

An Estate Plan is a Set of Formal Written Instructions for Your Family, Doctors, Courts and others regarding your:

Property

Finances

Family

It also empowers individuals to act on your behalf.

It keeps you in charge as long as you are alive and well.

It minimizes the need for guardianship or probate.

Authorizes a person that you choose to make decisions for you. If no power of attorney is in place and your are hospitalized or become unable to communication or make transactions, the agent you select will have that role. These may decisions about your finances, property, health and/or living situation.

If you do not have a Power of Attorney and become incapacitated, your family may not have the power to make critical decisions unless a court grants a guardianship. Read more here.

Advanced Healthcare Directives:

Instructs family and doctors about the care you want or don’t want at the end of your life.

It is followed when you are unable to speak for yourself.

Provides basic choices regarding lifesaving care, feeding tubes for food and hydration.

Can name a health care proxy to make other care decisions.

Having no Advanced Directive can cause family disagreements concerning your care and even end up in court.

Last Testament

Provides for payment of debts and expenses

Names a person to be in charge

Disposes of property left in your name

Requires a Court to admit it to probate

No Will (or other plan): Probate property will be distributed according to intestacy statutes and involve cumbersome probate procedures.

Trusts:

Avoids probate court

Can be changed

Can protect family from predators

Can protect assets from poor decisions

Provides inheritance

Works while you are alive

No Trust: Probate may be required to transfer titles to properties.

Transfer on Death

Vehicles, Minerals & Land

Avoids probate

Easy to set up

Inexpensive to create

Negative: Possible Disinheritance

Beneficiary Designations:

Life Insurance & Annuities

IRA, 401k, 403b other Retirement

Bank / Credit Union Accounts & CDs

Disadvantages: Limited Contingency

Estate Planning involves a skill set that identifies how property is held and how it is passed upon death. It also involves knowing what danger signs are ahead and how to plan for them. Knowledge of the formalities of various documents is a necessity to an effective estate plan.

The goals for most people is to stay in control as long as they are alive and well. When they’re not, a hand-picked trusted person follows your wishes and interests according to your “Rule Book”.

The main reason the people establish see an attorney about a Will or a Trust is to insure that their wishes, concerns and needs are met. It is best to prepare a plan is before it is needed. The problem is that none of us know exactly when or how this will occur.

Honored to receive the Award of Excellence from the Oklahoma Bar Association’s Estate Planning, Probate and Trust Section.

Our commitment to providing clear, honest guidance—treating every client with the same integrity I would show a member of my own family—is reflected in my AV Preeminent® peer review rating from Martindale-Hubbell.

This rating is the highest distinction a lawyer can achieve and is a testament to the fact that my fellow attorneys and members of the judiciary rank my work at the highest level of professional excellence.*

Note on Ratings: AV®, AV Preeminent®, Martindale-Hubbell Distinguished and Martindale-Hubbell Notable are certification marks used under license in accordance with the Martindale-Hubbell certification procedures, standards and policies. Martindale-Hubbell® is the facilitator of a peer review rating process. Ratings reflect the anonymous opinions of members of the bar and the judiciary. Martindale-Hubbell® Peer Review Ratings™ fall into two categories – legal ability and general ethical standards. This is not a certification of any specialty.

This website uses cookies.

{kind=link}

{kind=link}